Top 10 Investments with 10% Returns

There are two things you need to know.

First, there's no such thing as a guaranteed return on investment. The stated returns of every asset class are based on its historical performance, and past performance does not guarantee future results.

Second, higher returns almost always come with higher risk. The assets that have the potential to generate 10%+ returns tend to be more volatile, less predictable, and more likely to experience significant drawdowns along the way.

So your goal should be to focus on the investments that have most consistently averaged those kinds of returns in the past, and to understand the tradeoffs that come with them. That means knowing what kind of volatility you're signing up for and whether it fits your time horizon and risk tolerance.

Those are the things I cover in this article. And as you'll see below, some assets have a far stronger track record of generating double-digit returns than others.

Here's my list of the 10 best investments to get a 10% return on your investment.

Summary of the best investments with 10% ROI

| Investment | Yield* | Risk level* | Timeframe |

| 1. Private credit | 14.76% | 3.5/5 | Short |

| 2. Stocks | 10.4% | 3/5 | Long |

| 3. Real estate | 8.94% | 2.5/5 | Long |

| 4. Private startups | varies | 4.5/5 | Long |

| 5. Paying off debt | varies | 0/5 | Immediate |

| 6. Fine art | 11.2% | 4/5 | Long |

| 7. Buying a business | varies | 4/5 | Long |

| 8. Cryptocurrency | varies | 5/5 | Medium-to-long |

| 9. Junk bonds | 6.75% | 3/5 | Medium-to-long |

| 10. Collectibles | varies | 3/5 | Medium-to-long |

*Disclaimer: I've given each investment below an overall rating, as well as a risk score of 0 (low) to 5 (high). These are personal opinions. Return information based on sources linked below. Actual results may vary. Be sure to conduct your own due diligence.

1. Private credit

- Overall rating:

- Risk level: 3.5/5

- Best for: Accredited investors who want short-term income and diversification outside of public markets

- Where to invest: Percent*

Unlike public corporations which can issue bonds on public markets or small businesses that can borrow from banks, mid-sized private companies often struggle to access traditional financing.

These companies borrow from private, non-bank lenders in a market known as "private credit."

Over the last ~15 years, private credit has grown into one of the most popular asset classes among investment banks, hedge funds, insurance companies, and other institutional investors.

And now, platforms like Percent have opened the door for accredited investors* to invest directly in private credit, too.

*You qualify as an accredited investor if you have $200,000 (individually) or $300,000 (jointly) in annual income or a net worth of $1,000,000, excluding your primary residence.

Because this type of financing is harder for companies to obtain, private borrowers must offer more attractive terms. On Percent, the averages as of March 2026 were:

- 14.76% average APY on matured deals

- 17.25-month average duration

- 3.70% default rate

However, as seen recently, this asset class is not without risk. If you decide to invest, remember that your money will be tied up for the length of the loan and defaults do happen.

Many investors prefer to build their own portfolios of individual deals and focus on asset-backed loans — loans secured by underlying assets such as equipment leases or auto loans — which have performed better than other types of private credit, like direct lending.

Why I'd choose it: Short-duration income and diversification outside of public markets.

*Disclosure: This is an affiliate link. We may receive compensation if you take action through it.

2. Stocks

- Overall rating:

- Risk level: 3/5

- Best for: Most investors

- Where to invest: Public*

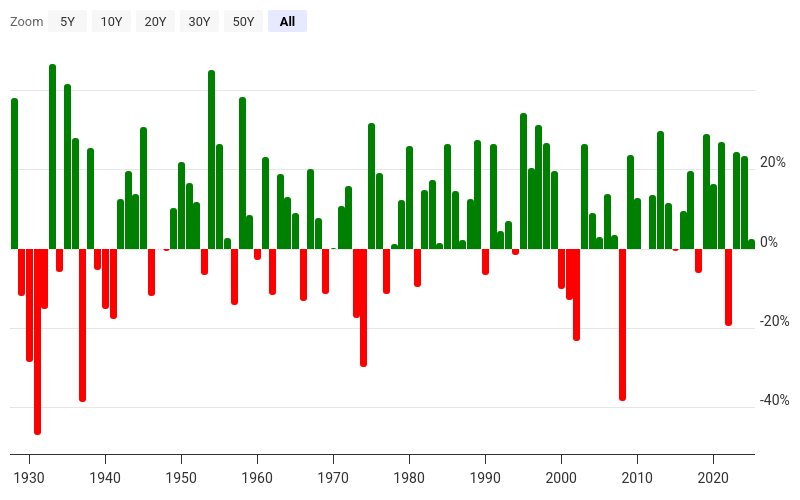

From 1926 to 2025, the S&P 500 returned 10.4% per year.

But that's just the average. As you can see in the chart below, annual returns vary widely. Some years the market is up 20% or more, while in others it's down just as much:

Source: Macrotrends

In reality, stocks almost never return 10% in a given year.

To actually capture those long-term returns, you need time. In most cases, that means staying invested for at least 5 to 10 years. The longer your time horizon, the more likely your returns are to resemble the market's historical average.

One of the simplest ways to invest in stocks is by buying an index fund. An index fund owns a large basket of stocks in a single investment, providing broad market exposure, high diversification, and low costs.

You can gain broad exposure to the S&P 500 by buying an index fund like VOO or SPY.

You can also invest in individual stocks, which can lead to higher returns.

However, it's more likely your performance will be worse picking individual stocks than buying index funds. Over a 10-year period, 91.4% of professional fund managers underperformed the market. If you try to beat the market (by buying individual stocks instead of index funds), the odds are stacked against you.

If you're interesting in getting stock picks with big upside potential, you may want to subscribe to a paid investing newsletter.

To invest in stocks & ETFs, you'll need a brokerage account. I like Public, which gives you access to stocks, ETFs, Treasuries, cryptocurrency, and other alternatives through a well-designed website and mobile app.

Why I'd choose it: Stocks are one of the most accessible asset classes and one of the most reliable ways to generate a 10% ROI (or higher).

*Disclosure: This is an affiliate link. We may receive compensation if you take action through it.

3. Real estate

- Overall rating:

- Risk level: 2.5/5

- Best for: Long-term investors who want to diversify their portfolios outside of public markets

- Where to invest: Arrived* or Fundrise*

Real estate has long been one of the most reliable ways to build wealth.

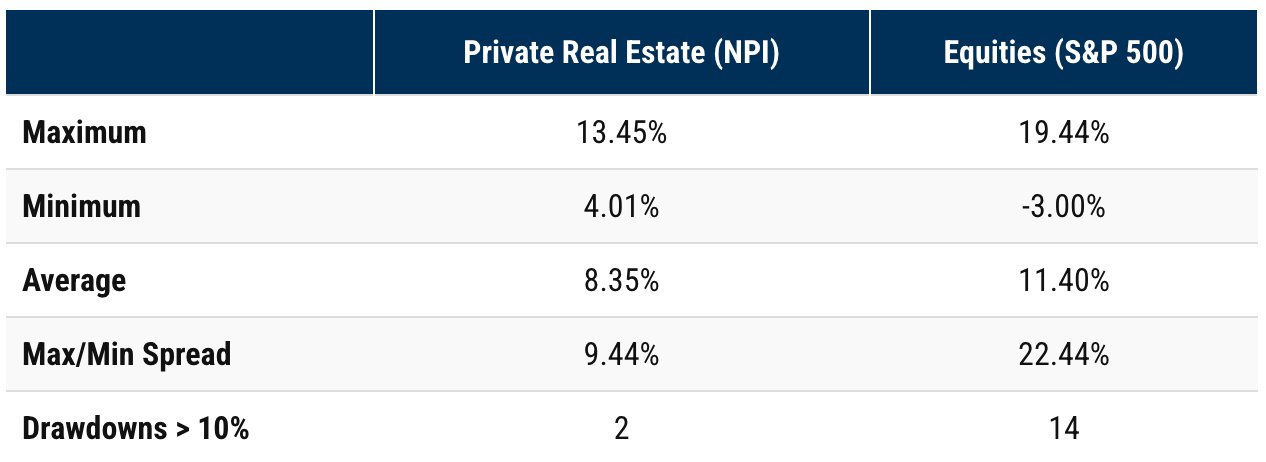

From 1978 to 2023, private real estate returned an average of 8.35% per year. While that trailed the S&P 500 by roughly 3%, it did so with much lower volatility:

Source: Bluerock

Real estate also offers multiple ways to generate returns: price appreciation, rental income, and tax advantages (like depreciation deductions and 1031 exchanges)

The main drawback is the upfront capital required to buy property. Most banks require 25% down payments on investment properties — that's $125,000 on a $500,000 house.

Fortunately, real estate crowdfunding platforms have made it much easier to get started. These platforms pool money from many investors to purchase and manage real estate on their behalf.

Two of my favorite options are Arrived and Fundrise:

- Arrived focuses on single-family homes used for both long-term and short-term rentals. In Q1 2026, its long-term rental properties paid annualized yields up to 9.9%.

- Fundrise invests across single-family rentals, multi-family apartments, and industrial assets. Its portfolio now exceeds $7 billion in value and includes more than 2.1 million investors.

Both Arrived and Fundrise are available to all investors. Their minimum investments are $100 and $10, respectively.

Why I'd choose it: Real estate has a proven track record of creating wealth while providing consistent income. It's also more stable than the stock market, making it a good asset for diversifying a portfolio.

*Disclosure: These are affiliate links. We may receive compensation if you take action through them.

4. Private startups

- Overall rating:

- Risk level: 4.5/5

- Best for: Accredited investors who want to invest in private, VC-backed companies

- Where to invest: Hiive* and Forge*

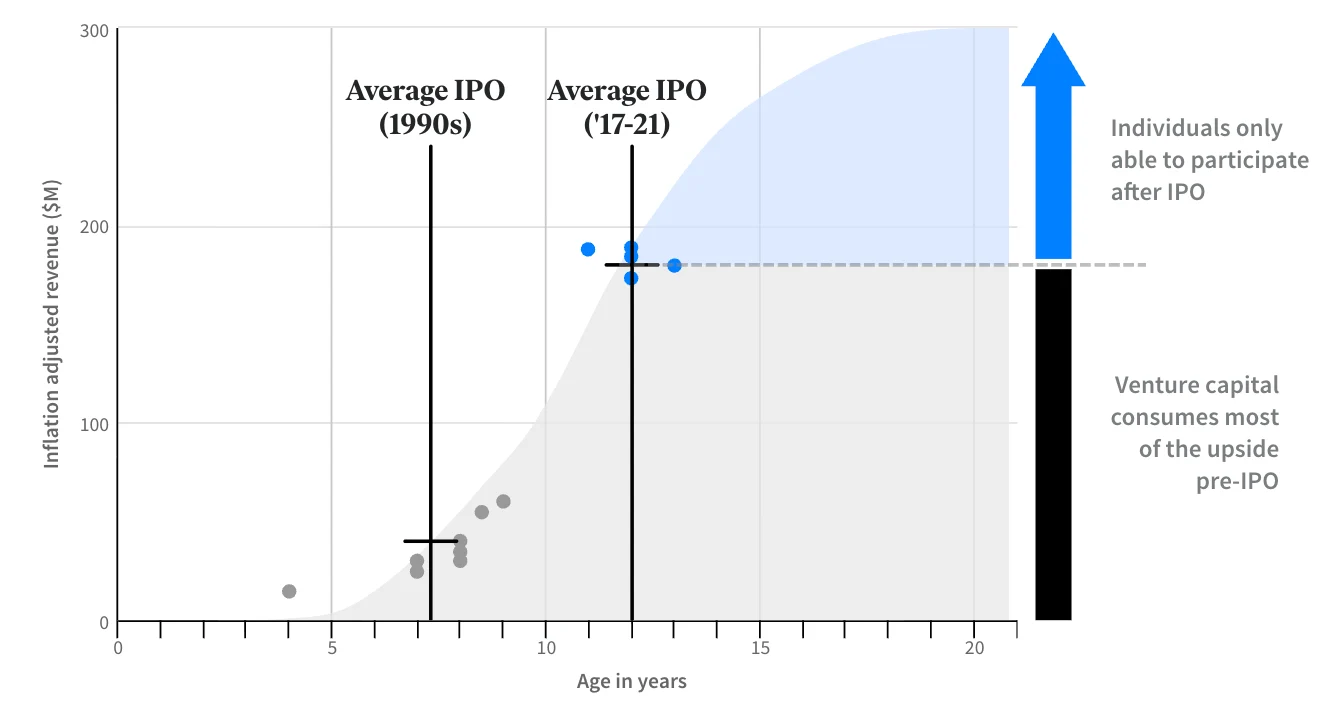

As private equity and venture capital investors know, more and more of the real money is being made before a company's IPO, not after.

Source: Fundrise

Companies are staying private longer, which means more of the returns are accruing in private markets.

Until recently, only institutional investors and insiders had access to these opportunities. Platforms like Hiive and Forge are changing that.

Hiive and Forge are pre-IPO marketplaces where accredited investors can buy shares of private companies. There are thousands of privately-held, VC-backed startups on these platforms, including SpaceX, Anthropic, and Databricks.

Investing in private startups is risky. The businesses are still developing, valuations are usually high and volatile, and liquidity is limited.

But for those with large enough portfolios and the ability to handle that uncertainty, it can offer unique upside.

Why I'd choose it: For accredited investors comfortable with making high-risk, high-reward investments, investing in private companies offers the chance to gain early stakes in the next generation of breakout businesses.

*Disclosure: These are affiliate links. We may receive compensation if you take action through them.

5. Paying off high-interest debt

- Overall rating:

- Risk level: 0/5

- Best for: Those with credit card or other high-interest consumer debt

- Where to invest: Your own credit card(s)

This one isn't technically an “investment,” but it deserves to be on this list.

If you're carrying a credit card balance with a 21% APR, paying it off is equivalent to earning a 21% rate of return. And that return is guaranteed.

It's surprising how many people start investing while still holding credit card debt. Other than taking advantage of a 401(k) employer match, there's no higher or more guaranteed return on investment than paying down high-interest loans.

My rule of thumb: If you have any debt with an interest rate above 7–8%, it usually makes sense to eliminate that debt before investing.

Why I'd choose it: Paying off high-interest debt is the highest guaranteed return on investment you could make.

6. Fine art

- Overall rating:

- Risk level: 4/5

- Best for: Investors who want diversification outside public markets through a tangible asset with a decades-long track record

- Where to invest: Masterworks*

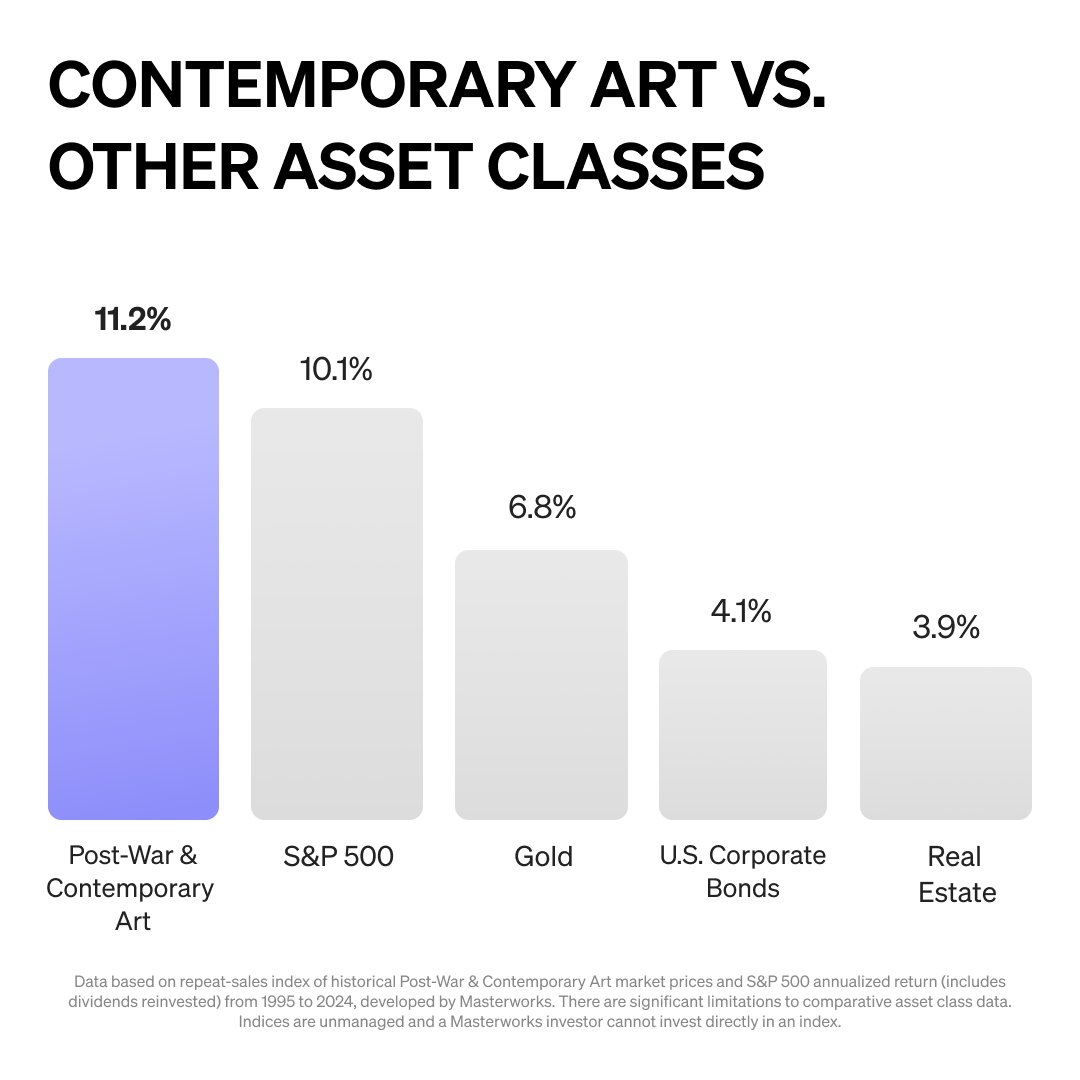

From 1995 to 2024, Post-War and Contemporary Art returned an average of 11.2% per year, outpacing the S&P 500, golf, corporate bonds, and real estate:

Source: Masterworks, The Masterworks All Art Index

Art has also proven to be one of the strongest inflation hedges available. During periods of elevated inflation, contemporary art sold at auction posted an average gain of 13.5%, compared to just 5.5% for stocks over the same periods.

And unlike most assets on this list, art prices show almost zero correlation with the stock market (0.09 vs. developed market equities), meaning it can hold its value even when equities are falling.

Similar to real estate, art investing historically has required millions of dollars and, as such, only been available to the ultra-wealthy. But platforms like Masterworks — a crowdfunding art investing platform — changed that.

Its team identifies which artists and paintings are gaining momentum, acquires the pieces, and then “securitizes” them — allowing users to buy fractional shares (starting at $20 each) in individual paintings.

The biggest downside: art is illiquid. Masterworks typically holds each piece for 3-10 years, and while a secondary trading market exists, liquidity is limited. This is best suited for patient, long-term investors.

Why I'd choose it: Art is another asset class with strong historical returns, near-zero correlation with stocks , and proven inflation protection. If you can commit capital for several years, it's one of the most unique diversifiers available.

*Disclosure: This is an affiliate link. We may receive compensation if you take action through it.

7. Buying a business

- Overall rating:

- Risk level: 4/5

- Best for: Anybody willing to take on the risk and extra work of owning a business

- Where to invest: LoopNet, Craigslist, and Flippa

When most people think about investing, they rarely consider buying an existing business.

Many local businesses sell for between 2–5x annual profits. That implies a 20–50% annual return, assuming the company's profits remain stable.

Unlike stocks or bonds, owning a business gives you direct control over performance. You can increase revenue, improve operations, or expand margins, all of which can dramatically raise the value of your investment.

Of course, it's not easy. Buying and running a business is far less passive than owning shares or real estate property. It requires more time, work, skill, and emotional bandwidth — and entrepreneurship simply isn't for everyone.

Plus, like real estate, it can be capital-intensive and lead you to idiosyncratic risk (having a large amount of money tied up in a single investment).

If you're interested, you can find businesses for sale on sites like LoopNet, Craigslist, or Flippa. You can also walk into a local business and ask the owner if they're open to selling or will be in the future.

Why I'd choose it: For those willing to get hands-on, buying a business gives you control over your investment's outcome, and can lead to huge ROIs.

8. Cryptocurrency

- Overall rating:

- Risk level: 5/5

- Best for: Believers in cryptocurrency and blockchain technology who don't mind the speculative nature of the asset class

- Where to invest: Public* and Coinbase*

Cryptocurrency exploded onto the scene a few years ago, after Bitcoin surged from around $3,500 in 2019 to over $60,000 in 2021. Today, Bitcoin trades above $80,000.

Since then, crypto has become one of the most popular investments among those seeking high returns.

However, digital currencies remain highly speculative.

Unlike a stock, which represents ownership in a company generating revenue and profits, cryptocurrencies aren't backed by underlying assets or cash flows.

The only way for investors to earn a profit from crypto is to sell it to another investor at a higher price. This investor, in turn, expects to sell it to another investor at a higher price in the future. This dynamic, known as The Greater Fool Theory, often leads to massive swings in price.

Personally, I don't invest in crypto. But for those who deeply understand specific coins, projects, or macro events that could impact prices, it may make sense to allocate a small percentage of your portfolio to the asset class.

Why I'd choose it: If you believe cryptocurrency will play a larger role in the global financial system, you may consider allocating a modest portion of your portfolio to crypto.

Be aware that the crypto space is full of scams, and there is a history of major crypto platforms going bankrupt.

For this reason, it's recommended to invest in crypto through a trusted platform that is regulated as a broker, like Public or Coinbase.

*Disclosure: These are affiliate links. We may receive compensation if you take action through them.

9. Junk bonds

- Overall rating:

- Risk level: 3/5

- Best for: Income-seeking investors comfortable with the risk/reward profiles of junk bonds

- Where to invest: Public*

Corporate debt generally falls into two categories: investment-grade and non-investment-grade, with the latter also known as "junk bonds."

Junk bonds are those with credit ratings below BBB/BAA, meaning the bond's issuer carries an elevated risk of default.

Junk bonds illustrate the classic risk-return tradeoff — the lowest-rated bonds pay the highest interest and are also most likely to default, and vice versa for higher-rated bonds.

Issuers of junk bonds offer higher interest rates to compensate investors for taking on the additional risk. Currently, junk bonds are paying about 7.11% interest, compared to around 5.56% interest on investment-grade bonds.

Since 2001, the average default rate for junk bonds has been around 3.5% per year. During the 2008 financial crisis, defaults climbed to 5.3% for the highest-rated junk bonds and over 13% for the most speculative debt.

While this might not seem high, that's more than one default out of every twenty bonds issued.

For most investors, buying individual junk bonds isn't practical due to the complexity and risk involved.

Instead, you can gain diversified exposure through a high-yield bond ETF, such as the SPDR Bloomberg High Yield ETF (JNK). You can buy this ETF in any brokerage account.

Why I'd choose it: For investors comfortable with higher risk, junk bonds can offer attractive yields and a steady stream of income — especially when used as a small, diversified slice of a balanced portfolio.

*Disclosure: This is an affiliate link. We may receive compensation if you take action through it.

10. Collectibles

- Overall rating:

- Risk level: 3/5

- Best for: Hobbyists or those with a particular affinity for a category of collectibles

- Where to invest: Locally, specialty websites, or eBay

I've developed a real appreciation for savvy collectors who deeply understand a specific niche — whether it's trains, coins, comic books, or sneakers — and can spot value when they see it.

Take one of my friends, for example.

He started collecting watches about ten years ago purely as a hobby. Today, it's the best-performing part of his portfolio. He's regularly doubling his money on watches and has never lost money on a watch he's purchased.

The best part? He enjoys it.

Collectible investing requires both passion and expertise. You need a sharp eye for value and a genuine obsession with the category. It's not for the faint of heart, or for those chasing quick profits.

But if you already have a deep interest in a particular area, it can make sense to dedicate a small portion of your portfolio to it.

Done right, collectibles can deliver strong, even outsized, returns — while being one of the few investments that's also fun.

Why I'd choose it: If I had a real edge in a collectible market, I'd absolutely make it part of my portfolio. With the right knowledge, you can earn exceptional returns and enjoy the process along the way.

How we chose the best investments with 10% ROIs

When evaluating investments, we consider the following:

- Returns: How has the investment performed historically? How is it expected to perform in the future? How stable/reliable are those returns expected to be?

- Risk: How much volatility should be expected? How much confidence can we place in the expected returns? How much downside is possible? How stable is the investment?

- Duration: How long should the investment timeline be? Should the investment be held for weeks, months, or years?

- Popularity: How popular is the asset among investors? Has the asset class been around for a long time, or is it relatively new?

- Accessibility: How easy is the investment to buy and sell? How simple is it to create an account and start investing? Are the recommended platforms easy to navigate?

Final verdict

That's my list of the 10 best investments with the potential to earn you a 10% ROI or more.

Just remember: Every investment comes with its own balance of risk and reward. Chasing higher returns often means accepting greater volatility and the possibility of loss.

The best way to manage that risk is by diversifying your portfolio, staying invested for the long term, and doing proper due diligence before you make an investment.

Any views expressed here do not necessarily reflect the views of Hiive Markets Limited ("Hiive") or any of its affiliates. Stock Analysis is not a broker-dealer or investment adviser. This communication is for informational purposes only and is not a recommendation, solicitation, or research report relating to any investment strategy, security, or digital asset. All investments involve risk, including the potential loss of principal, and past performance does not guarantee future results. Additionally, there is no guarantee that any statements or opinions provided herein will prove to be correct. Stock Analysis may be compensated for user activity resulting from readers clicking on Hiive affiliate links. Hiive is a registered broker-dealer and a member of FINRA / SIPC. Find Hiive on BrokerCheck.

.png)

.png)